Most people assume that handing a parcel to a courier means it's protected. It isn't. What is shipping insurance, exactly, and why does it exist separately from what carriers already offer? The answer matters more than most shippers realize. Carrier liability is capped, often well below the actual value of your goods. Declared value gives you a slightly higher limit, but it still isn't the same as real insurance coverage. This article breaks down how shipping insurance works, what it actually covers, what different policy types exist, and how to file a claim if something goes wrong.

Table of Contents

- Key Takeaways

- What is shipping insurance?

- Types of shipping insurance coverage

- How shipping insurance works: process, costs, and claims

- When and why shipping insurance matters

- Comparing your coverage options

- My honest take on shipping insurance

- Ship with confidence using Simplyparcel

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Shipping insurance covers more | It reimburses loss, damage, or theft beyond what carrier liability limits allow. |

| Declared value has real limits | Declaring a value raises the carrier's liability cap but does not provide all-risk protection. |

| Three coverage tiers exist | ICC Clause A, B, and C offer different levels of protection based on risk and shipment value. |

| Proper packing affects claims | Damage caused by poor packaging can void your claim, so packing quality matters as much as the policy. |

| Claims require documentation | Filing quickly with the right forms and receipts directly affects whether your claim gets approved. |

What is shipping insurance?

Shipping insurance is a financial protection product that reimburses you for the value of goods that are lost, damaged, or stolen during transit. Cargo insurance covers full cargo value regardless of carrier fault, and it protects against risks such as accidents, theft, and natural disasters. That last part is significant. Carrier liability, by contrast, only kicks in when the carrier is at fault and is subject to strict caps.

Understanding the difference between three terms will save you a lot of money and frustration.

Declared value is a figure you provide to the carrier when you book a shipment. Declared value sets a cap on the carrier's maximum liability, often calculated per pound or kilogram. It is not insurance. It simply tells the carrier how much they are on the hook for if something goes wrong under their own terms.

Carrier liability is the baseline protection every courier extends automatically. The problem is how low those limits go. Carrier liability may be capped at 2 SDR per kilogram under standard bill of lading rules. For a 10-kilogram parcel worth $2,000, that cap could leave you with a payout of roughly $27. That is not a safety net.

Shipping insurance, the actual product, is what fills the gap. It is typically purchased separately, either through your carrier, a freight forwarder, or a third-party insurer. It covers the actual commercial value of your goods and applies across a far broader set of risk scenarios.

| Coverage Type | What It Covers | Payout Basis | Cost |

|---|---|---|---|

| Carrier liability | Carrier's fault only, with strict caps | Weight-based formula | Included in shipping fee |

| Declared value | Extends carrier's liability cap | Declared amount, subject to terms | Small surcharge per shipment |

| Shipping insurance | Loss, damage, theft, broader perils | Full insured value | Percentage of cargo value |

Pro Tip: If you are shipping goods worth more than a few hundred dollars, always compare the carrier's maximum liability payout against the item's replacement cost before deciding whether to purchase shipping insurance.

Types of shipping insurance coverage

Not all shipping insurance policies work the same way. The broadest framework for understanding them comes from the Institute Cargo Clauses (ICC), which are the international standard for marine cargo insurance. They apply beyond ocean freight and are referenced widely in global shipping policies.

ICC Clause A, B, and C offer different levels of protection based on the scope of risk covered:

- ICC Clause A (all risks): This is the most comprehensive tier. It covers almost all accidental loss or damage unless specifically excluded. If something happens to your cargo and no exclusion applies, you are covered. This is the right choice for high-value, fragile, or irreplaceable goods.

- ICC Clause B (named perils, intermediate): This covers a defined list of risks including earthquake, volcanic activity, lightning, washing overboard, and some water damage. It does not cover theft or deliberate damage by third parties. It suits mid-value shipments where the specific named risks are the primary concern.

- ICC Clause C (basic coverage): This is the most limited tier. It protects only against major perils such as fire, explosion, sinking, and collision. Theft, breakage, and most accidental damage are not included. It works for low-value bulk cargo where the main worry is catastrophic loss.

Beyond the ICC framework, you will also encounter the terms all-risk coverage and named peril coverage in non-marine policies. All-risk coverage mirrors Clause A logic. Named peril coverage mirrors Clause B or C, listing only the events that qualify for a claim.

One exclusion that catches many shippers off guard is the packing insufficiency rule. Damage claims can be denied if the insurer can prove that insufficient packaging by the insured's employees was the direct cause of the loss. The burden of proof sits with the insurer, not with you, but it is still a risk worth eliminating by packing correctly in the first place. For guidance on packaging standards for transit, checking industry benchmarks before you ship is a smart practice.

Choose your coverage tier based on two factors: the replacement value of your goods and your tolerance for partial loss. If you cannot afford to absorb any loss, go with all-risk coverage.

How shipping insurance works: process, costs, and claims

Shipping insurance explained in practical terms comes down to three steps: buying the policy, paying for it, and knowing how to claim if needed.

Buying coverage happens at booking. You declare the commercial value of your goods, choose a coverage level, and the premium is calculated. Most carriers and platforms allow you to add insurance at checkout. Third-party insurers often offer broader coverage at better rates for frequent shippers.

The cost of shipping insurance is typically a percentage of the declared cargo value, usually between 0.5% and 3%, depending on the commodity, destination, carrier, and coverage tier. Fragile goods, electronics, and international routes tend to push the rate higher. For a $1,000 parcel, expect to pay between $5 and $30 in insurance premiums.

Filing a claim is where preparation pays off. Follow these steps to give your claim the best chance of approval:

- Document the damage immediately. Take clear photos of the parcel, packaging, and any damaged items the moment you notice an issue. Do not discard the packaging.

- File on time. Different carriers have different windows. For USPS shipments, damaged or missing contents must be reported immediately. Waiting too long can disqualify your claim entirely.

- Gather your paperwork. You will need original mailing receipts, proof of value (receipt or invoice), and carrier-specific forms. For international insured USPS parcels, forms like PS Form 2856 are required.

- Submit a formal inquiry first if required. Some carriers require a lost parcel inquiry before they accept a formal claim. Check your carrier's process before jumping straight to a claim form.

- Keep copies of everything. Retain all correspondence, receipts, and submitted forms. Starting documentation early supports claim approvals and gives you a paper trail if there is a dispute.

Pro Tip: Never ship a high-value item without printing the insurance confirmation and storing it alongside your mailing receipt. If a claim arises weeks later, having that documentation on hand removes a major hurdle.

When and why shipping insurance matters

The risks of transit are real and consistent. Parcels get lost in sorting facilities, crushed in transit, stolen from delivery points, or damaged by moisture. Here are the situations where shipping insurance stops being optional and starts being necessary:

- High-value shipments. Electronics, jewelry, branded goods, and collectibles are worth far more than any carrier will reimburse under standard liability. A single lost package can represent a significant financial loss without insurance.

- Fragile items. Glassware, ceramics, art, and instruments can be damaged even with good packaging. Insurance does not replace careful packing, but it does protect you when damage happens despite your best efforts.

- International shipments. Cross-border shipping introduces more handling points, customs clearance risk, and longer transit times. Each additional touchpoint adds risk. For international parcel shipping, adequate coverage is especially worth the cost.

- E-commerce businesses. A business shipping dozens of orders weekly cannot absorb the occasional lost or damaged parcel as a routine operating cost. Insurance converts an unpredictable loss into a manageable, fixed expense.

- Gifts and personal items. Sentimental value aside, replacing personal items out of pocket adds up quickly. Many people underestimate how costly replacing everyday items can be when they are no longer under warranty.

The cost-versus-risk calculation is straightforward. If the insurance premium represents a small fraction of the item's replacement cost, and the risk of loss or damage is non-trivial, coverage makes financial sense. Full coverage requires an all-risks insurance policy rather than relying on declared value alone, particularly for goods where replacement cost is high.

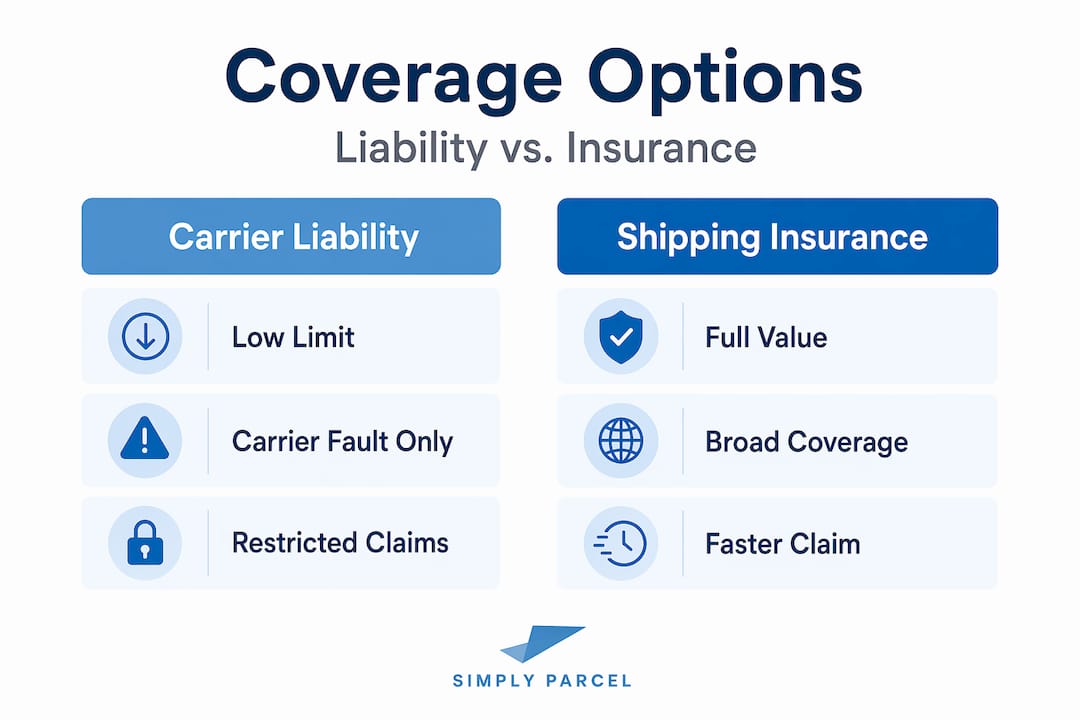

Comparing your coverage options

Before you ship, it helps to see all three protection options side by side. This is shipping insurance explained in its simplest form.

| Option | Coverage scope | Best for | Claim rights |

|---|---|---|---|

| Carrier liability | Carrier's fault, capped by weight | Low-value, non-fragile goods | Limited, carrier-controlled |

| Declared value | Raises carrier's liability ceiling | Mid-value goods, trusted routes | Subject to carrier's terms |

| Shipping insurance | Loss, damage, theft, broader perils | High-value, fragile, international goods | Independent claims process |

The key insight here is that declared value and shipping insurance operate as distinct systems. Declared value raises the ceiling on what a carrier owes you. Shipping insurance replaces that ceiling with comprehensive coverage across a much wider set of scenarios. When the cost of your goods exceeds a few hundred dollars, the case for full insurance is clear.

My honest take on shipping insurance

I've watched shippers make the same mistake repeatedly. They declare a value, assume they're covered, and then discover after a loss that the carrier's payout covers a fraction of what they're owed.

What I've learned from handling claims and watching shipments go wrong is this: declared value is a liability cap, not a safety net. It gives you a slightly higher ceiling on what a carrier admits to owing you. It does not protect you from the full range of ways a parcel can be lost or damaged in transit.

My recommendation for anyone asking "do I need shipping insurance" is to think about it from a replacement cost perspective. If you would feel the financial impact of losing that parcel, buy the insurance. The premium is almost always smaller than people expect.

The thing that rarely gets mentioned alongside insurance advice is packaging. I've seen claims denied because the damage was traced back to insufficient packing, even when the insurer had to prove it. You can have the right policy and still lose a claim because the box wasn't up to standard. Insurance and packing quality go together. Neither replaces the other.

One more thing worth saying: third-party insurance providers often offer better rates and broader terms than carrier-issued coverage. If you ship regularly, comparing those options saves real money over time. You can also use parcel tracking alongside insurance to catch problems early and build a stronger claims record.

— Simply

Ship with confidence using Simplyparcel

Simplyparcel makes it straightforward to book insured international shipments from Singapore, whether you're an individual sending a gift abroad or a business managing regular exports. Through the platform, you can compare courier options, declare your shipment value, and access insurance coverage without dealing with multiple providers. Simplyparcel works with major courier partners to give you transparent pricing and real-time tracking on every parcel. If you want to see your options before committing, you can get an instant quote and review available coverage levels for your specific destination and parcel type. Protecting your shipment starts before the parcel leaves your hands.

FAQ

What does shipping insurance cover?

Shipping insurance covers financial loss from goods that are lost, damaged, or stolen during transit. Depending on the policy, it may cover accidents, theft, and natural disasters, and it pays out based on the declared commercial value of your goods.

Is shipping insurance the same as declared value?

No. Declared value raises the carrier's liability cap but does not provide full insurance protection. True shipping insurance offers broader coverage across more risk scenarios and operates independently of carrier liability terms.

How much does shipping insurance cost?

Shipping insurance typically costs between 0.5% and 3% of the declared cargo value. The exact rate depends on the commodity type, destination, carrier, and level of coverage selected.

Do I need shipping insurance for every parcel?

Not necessarily. For low-value, non-fragile goods on short domestic routes, carrier liability may be sufficient. For high-value items, fragile goods, or international shipments, purchasing shipping insurance is strongly recommended.

Can a claim be denied even with insurance?

Yes. Claims can be denied if the damage was caused by insufficient packaging on the shipper's part. Filing promptly with complete documentation, including photos, receipts, and carrier forms, gives your claim the strongest possible foundation.